[ad_1]

This articles features insights from one of AgFunder’s international data partners, who provide data for AgFunder’s agrifoodtech investment reports. AgFunder is AFN’s parent company.

Click here for more research from AgFunder and sign up to our newsletters to receive alerts about new research reports.

China maintained its silver-medal position as the world’s second-largest agrifoodtech investment destination in 2021, according to AgFunder’s most recent Agrifoodtech Investment Report.

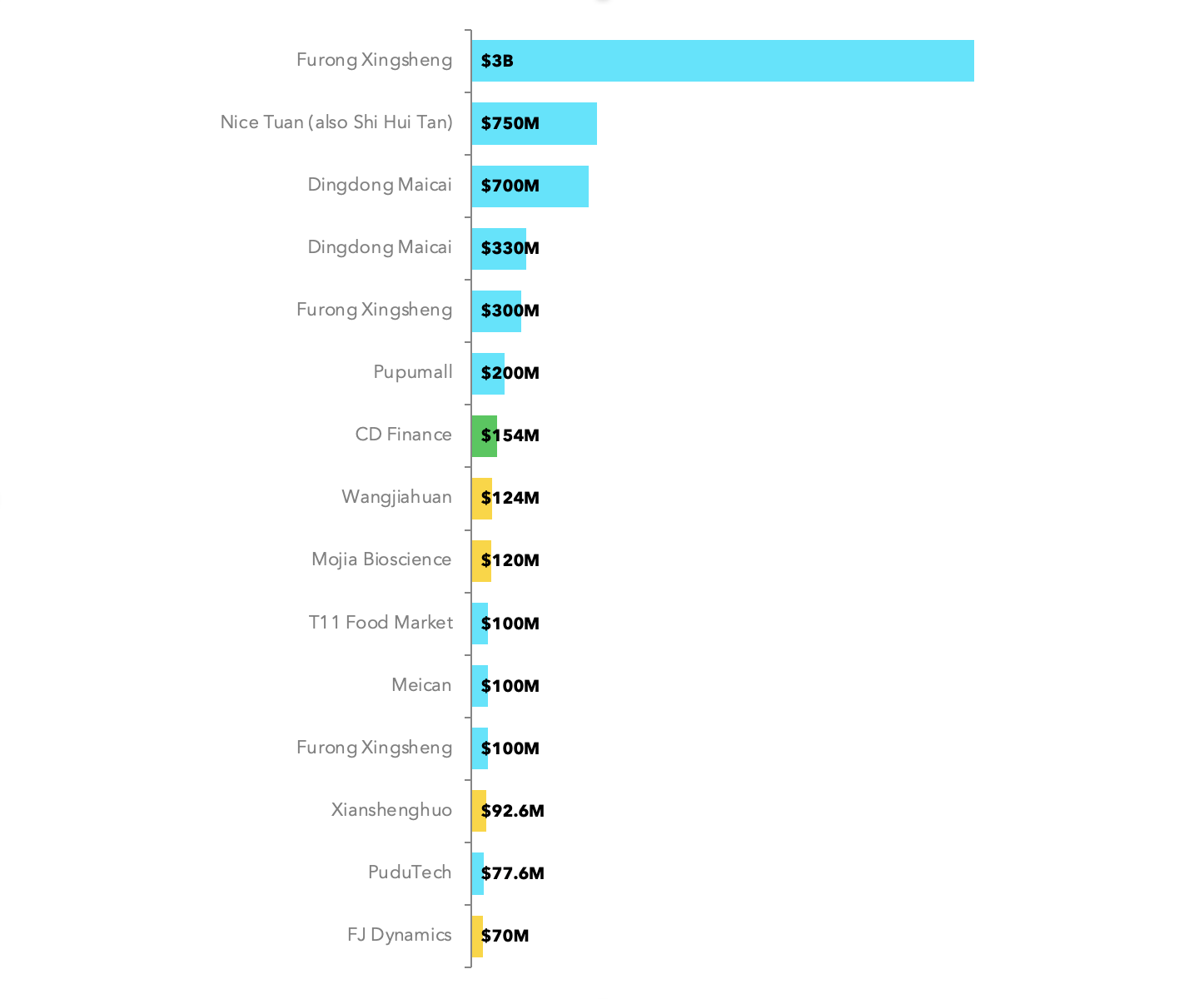

China’s top 15 agrifoodtech venture deals, 2021

Chinese agrifoodtech ventures raised a total of $7.3 billion last year, behind only the US’s $21 billion.

Of that $7.3 billion, 75% went to startups in the eGrocery category. In fact, China’s six biggest agrifoodtech deals last year involved four eGrocery platforms. This included China’s — and the world’s — top agrifoodtech funding round of 2021: Furong Xingsheng‘s $3 billion raise in February from investors including Sequoia Capital, Temasek, Tencent, and KKR.

The country’s biggest category by deal count, on the other hand, was Midstream Technologies (32 deals). However, the sector raised only about $400 million – or 5.5% of China-bound capital. Two Midstream Tech companies were among the top 15 deals; ag produce distributor Wangjiahuan and cold chain solutions provider Xianshenghuo.

Other startups appearing in the top 15 included rural fintech platform CD Finance and farm robotics specialist FJ Dynamics.

Here, Winnie Leung (WL), vice president at our China data partner Bits x Bites, digs down into the data.

What do China’s top 15 deals in 2021 tell us about the broader agrifood venture funding landscape?

WL: Downstream deals dominate China’s agrifood investment scene. This year’s top deals exemplify that, thanks to the backing of cross-sector investors from the TMT and consumer sectors. Yet these deals don’t reflect the amount of disruption expected upstream.

In 2017, upstream deals were just 6% of total funding. They surged to more than 20% in the past two years. When you consider China is the second-largest agrifoodtech investing market, this shift is significant. We expect the gap will continue to close.

Overall, what were the key trends and developments in agrifood venture funding in your region in 2021?

WL: Few priorities are higher in the Chinese government agenda than food self-sufficiency and carbon neutrality. After two decades of farmland consolidation, larger field operations now have the scale and skills to use precision ag solutions to boost yield and manage inputs. The safety certificates recently issued to local Chinese breeds of GM soy and corn are taking us one step closer to local GM crop farming and triggering breeding innovations. Tightening environmental regulations for chemical production have effectively boosted biomanufacturing of essential nutrients.

It’s worth watching how companies developing farm management software and ag biotechnology will use these top-down forces to their advantage and grow.

What are your expectations for 2022?

WL: 2022 will be the year of biotechnology.

China has cost and supply chain advantages in fermentation. As the demand for capacity grows alongside continued fermented protein innovation, China is in a good position to push the pedal. The country’s 14th Five-Year Plan for agriculture set goals to develop cellular agriculture and synthetic dairy for the first time; this gives yet another reason to follow how this happy collision of factors will unfold.

[ad_2]

Source link